Executives across the payments and lending spectrum have used their second-quarter earnings calls to emphasize embedded finance not just as a future prospect, but as a present-day growth engine.

Embedded finance broadly refers to payments or banking functions built into non-financial enterprises and platforms, while embedded lending narrows the definition to credit offered directly at checkout or within a workflow. Both figured prominently in comments and results across a broad range of players, indicating a shift in how financial services are distributed.

Networks: Embedding Into Platforms

Visa’s Q3 FY 2025 remarks from CEO Ryan McInerney highlighted platform solutions including card-as-a-service and payouts which offer “credit and debit card issuance, product lifecycle management and digital accounts to businesses across agribusiness, real estate, auto and retail.”

Mastercard’s Q2 2025 earnings review emphasized virtual cards and data services wired into enterprise software, positioning itself as an embedded partner in corporate payments.

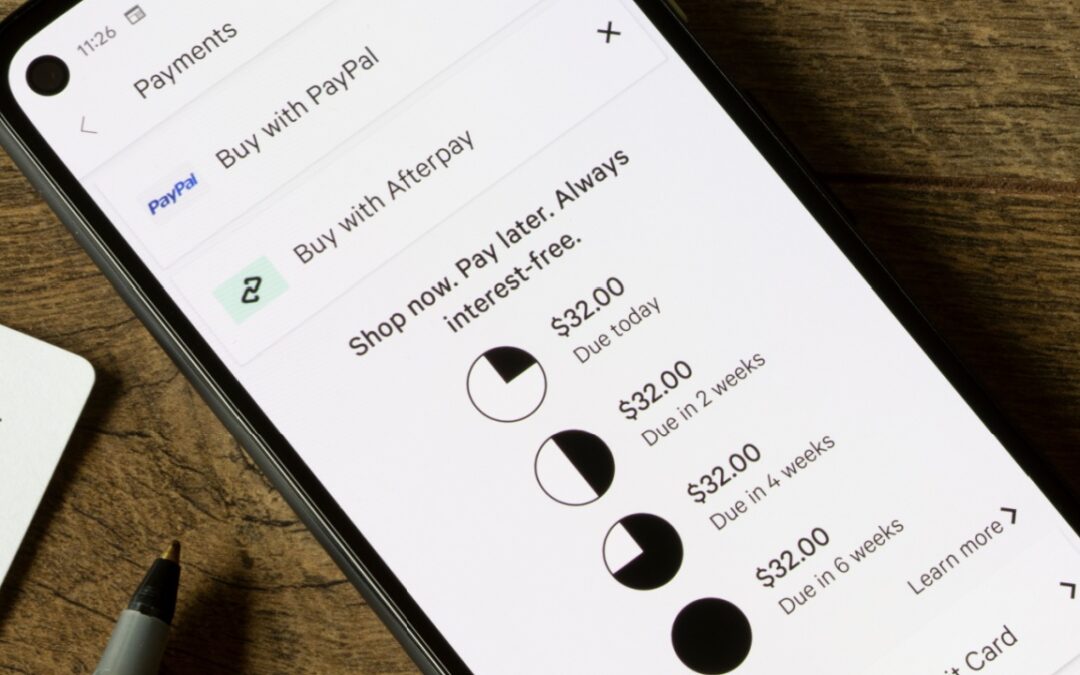

PayPal’s Q2 2025 call details indicated the growth in lending, as the company ended the quarter with $6.9 billion in net loan receivables, where growth came from the company’s buy now, pay later loans. Those loans are delivered inside PayPal’s checkout button and apps, illustrating the growth in embedded lending at the exact moment of purchase.

Block’s shareholder letter and prepared remarks underscored Afterpay’s role in merchant conversion and its integration across Square’s point-of-sale and online checkout. Afterpay is embedded directly into Square’s commerce stack, the company said, linking consumer demand for installments with merchant adoption.

Cash App, meanwhile, is layering financial services such as investing and savings into its app. As reported earlier this month, the company is personalizing Cash App Card offers and planning an “auto-selection” feature to help users unlock savings without extra effort. On the BNPL front, gross merchandise value hit $9.11 billion, up 17%, fueled by Pay-in-Four plans and new post-purchase options.

Fiserv’s Q2 2025 earnings call spotlighted its banking-as-a-service platform Finxact and the Clover point-of-sale system. And in remarks, CEO Mike Lyons said during the call, “We will integrate Vision Next with Finxact and Payfair to provide a unified next generation embedded finance solution. … Finxact continues to gain momentum with banks, FinTechs and embedded finance participants.”

Specialty Lenders, Issuer Processors

Upstart, in its Q2 2025 earnings call, described embedding underwriting directly inside auto dealerships and bank partners where management noted triple-digit growth in those business lines. CEO Dave Girouard said on the call that “the dealership adoption right now is like nothing we’ve seen in the past, and the volume of loan requests and closed agreements from our dealer partners is on a steep climb. This is a recent phenomenon.”

Marqeta’s Q2 2025 materials and comments also underscore the growth of embedding finance. The firm enables card issuance or payouts under client firms’ own brand, letting marketplaces and FinTechs embed banking services invisibly into their products. Management noted on the conference call with analysts that banking, lending, BNPL and expense management use cases are each growing over 100% year over year in Europe.

While headlines focused on margins and revenue beats, the repeated references to embedded finance suggest something deeper. Financial services are shifting from being marketed directly by banks or card issuers to being distributed through software platforms, marketplaces and digital ecosystems. Embedded lending, in particular, is gaining ground as consumers and businesses grow accustomed to credit being offered seamlessly at checkout or within the applications they already use.